Paramètres

En savoir plus sur le livre

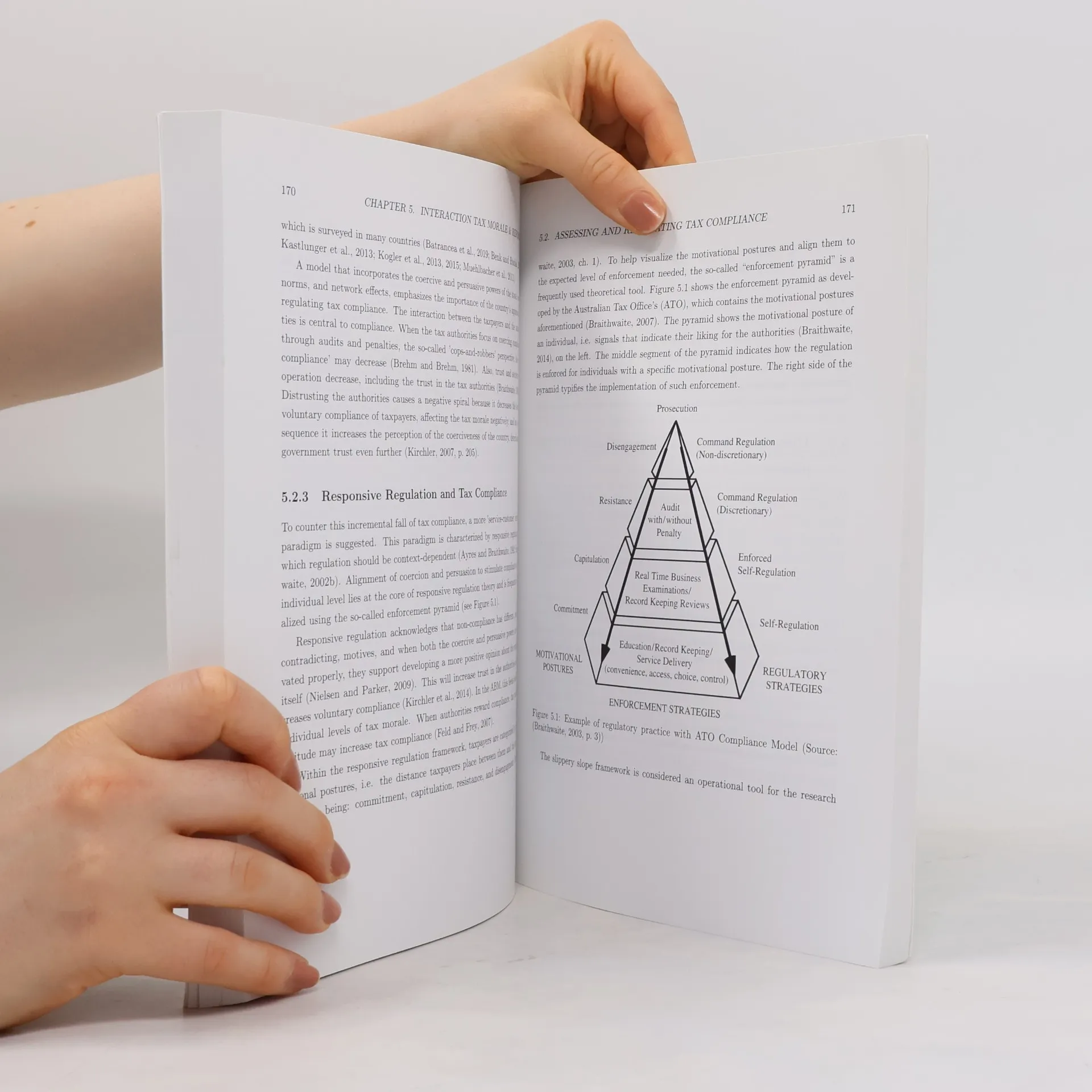

International mobility of individuals and businesses, along with new technologies, creates opportunities for tax avoidance and evasion. To maintain tax revenues, governments must offer an attractive tax environment, leading to competition among them. In response, new EU regulations, such as country-by-country reporting and automatic information exchange, have been implemented. This dissertation examines the impact of these regulations on tax evasion and avoidance using an agent-based simulation model that reflects the choices of individuals and businesses. Compliance is influenced by international legal and tax system differences and the information agents receive from their surroundings. While short-term effects of these regulations boost overall compliance, long-term outcomes may undermine their objectives. The research offers a framework to enhance tax compliance without intensifying tax competition over time. Attractive tax laws often provide financial secrecy, obscuring corporate ownership and revenue sources, which benefits not only tax evaders but also criminal organizations laundering illicit proceeds. Anti-money laundering regulations aim to address the risks associated with financial secrecy and influence criminal networks. This dissertation assesses the impact of such regulations on the structures of criminal organizations, demonstrating that while they complicate money laundering, they also inadvertently affect leg

Achat du livre

Tax Dynamics and Money Laundering, Peter Gerbrands

- Langue

- Année de publication

- 2021

- product-detail.submit-box.info.binding

- (rigide),

- État du livre

- Bon

- Prix

- 4,79 €

Modes de paiement

Personne n'a encore évalué .

- Titre

- Tax Dynamics and Money Laundering

- Sous-titre

- Simulating Policy Reforms in a Complex System

- Langue

- Néerlandais

- Auteurs

- Peter Gerbrands

- Éditeur

- Universiteit Utrecht

- Publié

- 2021

- Format

- rigide

- ISBN10

- 9491870459

- ISBN13

- 9789491870453

- Séries

- Mots clés

- Sciences sociales, Affaires & Gestion, Sciences politiques & Politique, Thématique juridique, Économie, Série Policier

- Description

- International mobility of individuals and businesses, along with new technologies, creates opportunities for tax avoidance and evasion. To maintain tax revenues, governments must offer an attractive tax environment, leading to competition among them. In response, new EU regulations, such as country-by-country reporting and automatic information exchange, have been implemented. This dissertation examines the impact of these regulations on tax evasion and avoidance using an agent-based simulation model that reflects the choices of individuals and businesses. Compliance is influenced by international legal and tax system differences and the information agents receive from their surroundings. While short-term effects of these regulations boost overall compliance, long-term outcomes may undermine their objectives. The research offers a framework to enhance tax compliance without intensifying tax competition over time. Attractive tax laws often provide financial secrecy, obscuring corporate ownership and revenue sources, which benefits not only tax evaders but also criminal organizations laundering illicit proceeds. Anti-money laundering regulations aim to address the risks associated with financial secrecy and influence criminal networks. This dissertation assesses the impact of such regulations on the structures of criminal organizations, demonstrating that while they complicate money laundering, they also inadvertently affect leg